Identity theft protection services seem to be everywhere these days, and it makes sense. Protecting your identity in a world where we hear about data breaches on a regular basis seems difficult without some help from somewhere.

To help you with your decision on deciding which ID theft protection service to choose, I will be breaking down two of the best-known names in this market: IdentityForce and LifeLock. Here at Comparitech, testing the strengths and weaknesses of identity theft protection services is part of our DNA. I will give you the information you need to know to determine whether LifeLock or IdentityForce will fit your needs better.

Don’t want to read the full IdentityForce vs LifeLock article?

Even though LifeLock and IdentityForce both offer plenty of desirable features, I will give the nod to LifeLock. It has strong features at its highest-priced tier, and its well-known brand name gives it a trustworthy feel that other ID theft protection services struggle to match. With IdentityForce, you receive a feature set at its lowest-priced tier that is more robust than what LifeLock offers for a similar price. However, I believe LifeLock matches the needs of more people.

Summary: IdentityForce vs LifeLock

| No value | Identity Force | LifeLock |

| Website | identityforce.com | https://lifelock.com/ | Free trial | Identity theft insurance | Up to $1 million | Up to $1 million | Lock your credit | TransUnion only | Special offer | $17.99 | $8.99 | Highest price per month | $23.99 | $23.99 | Credit monitoring | Crime in your name monitoring | Credit reports | Credit score |

|---|---|---|

| Best deal (per month) | Free trial Get a 14-day FREE trial! | $8.99 GET 25% off the first year |

IdentityForce vs LifeLock: Features

When comparing identity theft protection services, certain features will be more important for your personal needs than others. I put together a list of some of the most important features for the majority of customers. Use these comparisons to help you determine whether IdentityForce or LifeLock is the better option for your needs.

Activity alerts

Giving you alerts as to when strange activity occurs with your personal data or financial accounts is at the heart of all identity theft protection services. Both LifeLock and IdentityForce have solid features here, giving you warnings when something just isn’t right.

With both IdentityForce and LifeLock, you’ll receive monitoring and alerts for odd activity for your bank accounts, credit cards accounts, investment accounts, and Social Security Numbers.

Should a credit bureau find a change in your credit profile, you should receive notification from both LifeLock and IdentityForce (although you may need to subscribe to a higher-priced subscription tier with LifeLock for this alert). You also can choose how you would like to receive alerts from both services, such as via text or email.

IdentityForce and LifeLock both offer a feature that monitors your personal data for any payday loans opened in your name. This is a new feature with LifeLock, which offers this feature in its middle and upper pricing tiers.

Dark web monitoring

Dark web monitoring involves searching places like hacker forums and dark web marketplaces for personal information related to you, such as your mother’s maiden name, account passwords, or your debit card numbers. If someone is selling your personal information online, your chances of suffering identity theft increase significantly.

Both LifeLock and IdentityForce will perform dark web monitoring.

LifeLock will give you an alert when it finds your personal information through its dark web monitoring. IdentityForce performs an analysis of the data it discovers, trying to determine the actual risk to your identity. It then gives you a rating of your risk level, so you can decide how you want to proceed.

Free credit report and monitoring

Both services closely watch your credit profile, monitoring it for any odd activity that should give you notification of any attempts to open a credit line in your name. Monitoring of the use of your Social Security Number, which both services provide, also can help in this area.

With IdentityForce, you receive monitoring and reports from all three credit bureaus at either pricing tier. However, with LifeLock, you receive monitoring at one credit bureau in the two lower pricing tiers and at all three bureaus in its highest pricing tier.

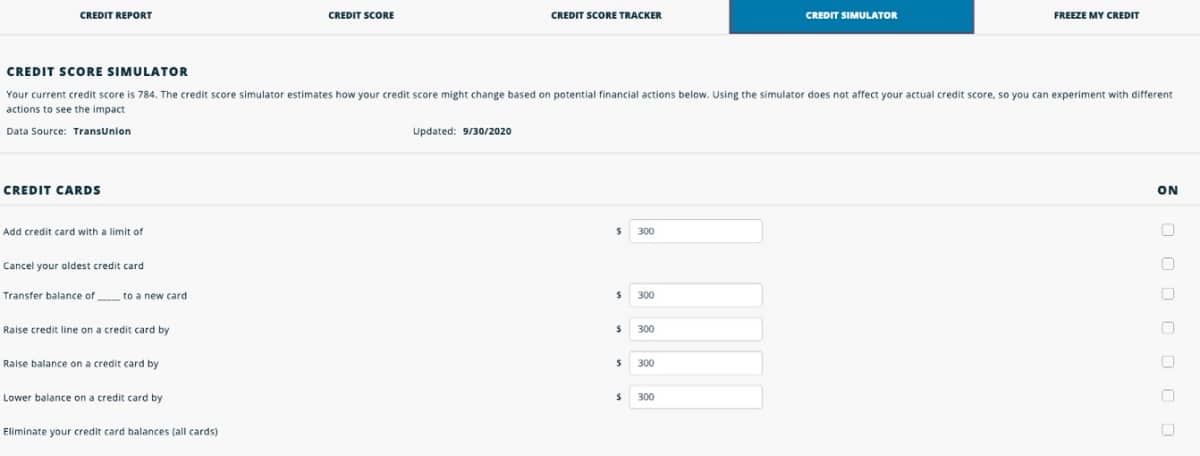

A handy feature found in both pricing tiers of IdentityForce is its Credit Score Simulator. This simulator will give you an idea of how different actions you take regarding credit card balances or payments could affect your credit score. I like this feature quite a bit, although some people will prefer a service that focuses solely on identity theft features, like LifeLock.

Both LifeLock and IdentityForce can help you freeze your credit with the credit reporting bureaus, if desired. This prevents anyone from opening a line of credit in your name. However, you will have to unfreeze your credit if you plan to try to open a new line of credit in the future.

Address monitoring

IdentityForce does not offer specific home title monitoring, but LifeLock recently added this feature in its highest-pricing tier. They both have other features that could help you spot a problem in this area quickly.

LifeLock and IdentityForce will monitor the use of your address, determining whether someone changed your physical address with the U.S. Postal Service. The hacker then could gain access to all of your bills and other personal mail, making it easier to attempt to steal your identity.

Public records monitoring

Both of these identity theft protection services will keep an eye on court records and sex offender registry lists, determining if anyone stole your identity and then suffered an arrest and a criminal charge.

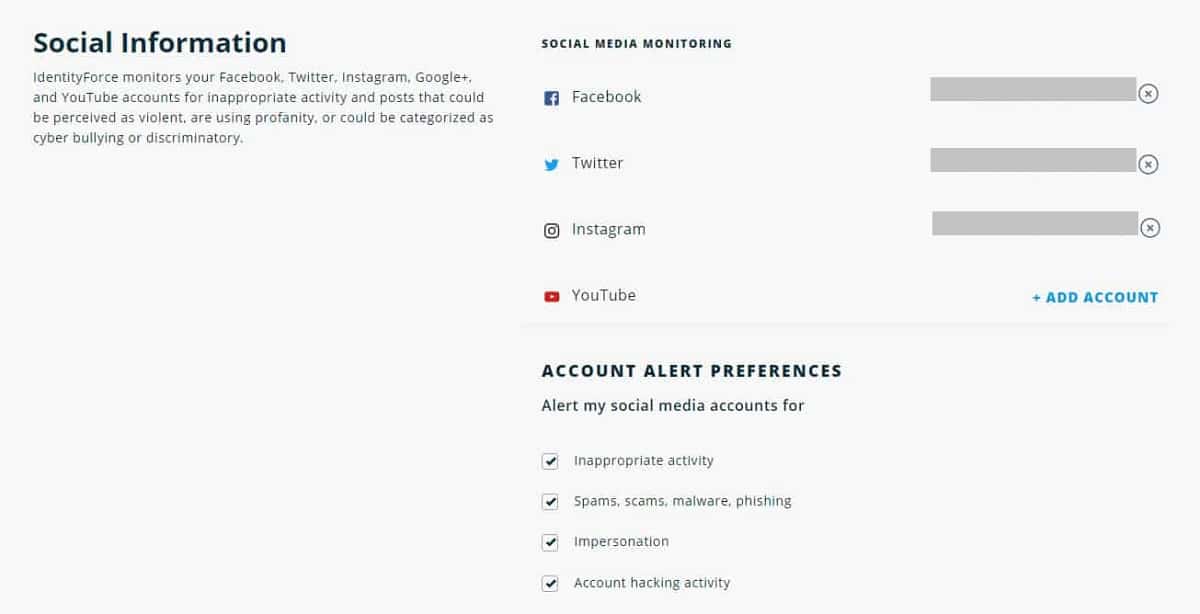

Social media monitoring

LifeLock and IdentityForce both offer the ability to track any social media accounts associated with your name, including Facebook, YouTube, and Instagram.

Someone could steal your social media passwords and impersonate you online. This hacker could make fake posts on your accounts or promote violence or cyberbullying. If so, these monitoring services can catch the problem quickly before your personal reputation suffers significant damage.

ID restoration

Because identity restoration is the most important aspect of identity theft protection services, it is important that both IdentityForce and LifeLock excel in this area. Both of them offer similar types of features to help you regain control of your identity as quickly as possible.

Both services can steer you toward lawyers and other experts to help you complete the paperwork necessary to restore your identity.

Although IdentityForce does not have customer service representatives available 24 hours a day and seven days a week like LifeLock does, IdentityForce does make its ID recovery experts available to you 24/7 when trying to help you recover your identity. LifeLock has 24/7 support in either situation.

Insurance and compensation

Both LifeLock and IdentityForce provide you with up to $1 million in insurance coverage related to the costs you will encounter while trying to restore your identity. This money is helpful in hiring lawyers and financial professionals to work on various aspects of restoring your identity.

This insurance money also helps you with any wages you lose while being unable to work during the time you are trying to restore your identity. Should you need child care or elder care while trying to restore your identity, the insurance money also will reimburse you with both services.

Should you lose personal funds to the identity thief, LifeLock offers you between $25,000 and $1 million in compensation, depending on your subscription tier.

IdentityForce offers up to $1 million in stolen funds replacement, but the exact amount you could receive will depend on the subscription tier you select. IdentityForce does not list the minimum amount you could receive in stolen funds reimbursement in each subscription tier, which I found to be a concerning omission on its part.

2FA login

Both LifeLock and IdentityForce offer two-factor authentication (2FA) for your account. However, you will have to enable 2FA with your account. It is not automatic.

IdentityForce vs LifeLock: Pricing

LifeLock offers significantly more pricing tiers than IdentityForce. This is an advantage when you want to find the perfect pricing tier for your budget and needs. However, it also brings a level of complexity into the process of selecting a pricing tier that IdentityForce’s simpler pricing structure does not have.

When comparing the two services, LifeLock’s most basic service is cheaper than IdentityForce’s most basic service. However, I still give IdentityForce the edge here, because its lowest-priced tier carries significantly more features than LifeLock’s lowest-priced tier. If you only want the cheapest service, then you can go with LifeLock. However, I much prefer the value that IdentityForce’s lowest-priced tier provides.

LifeLock offers a more significant discount for new customers for the first year than does IdentityForce. This will make LifeLock’s prices seem quite a bit lower than IdentityForce’s prices.

Remember, though, most people want an identity theft protection service that they can trust for many years. Always pay closer attention to what you will pay in future years than being tempted by a low introductory price.

Auto renewal options

Both LifeLock and IdentityForce use the same auto renewal policies. When you sign up for the service and provide a credit card or banking information, the terms of service become effective. By accepting these terms, you agree to allow LifeLock or IdentityForce to automatically charge you at the time of renewal.

Should your credit card or banking information in use with these services change, you will receive a notification that the service could not charge you. You then will have a chance to update your payment information. Failure to do so could lead to cancelation of your account and a purging of your stored alert data.

If you do not cancel your account before the date of renewal of your subscription, you will receive a charge for the entire next subscription period.

Cancellation options

When canceling your subscription, you can call or visit the IdentityForce or LifeLock websites. Although these services make canceling seem easy, it may require multiple phone calls and follow up emails.

We should note that IdentityForce does not accept cancellation requests by phone outside of normal business hours, further complicating the process. Because of this delay, you could end up receiving a charge for the next subscription period while you are attempting to cancel.

Before signing up for either service, thoroughly read the LifeLock terms of service and the IdentityForce terms of service for the latest information, as these terms are subject to change.

During my LifeLock hands-on review, I actually had a relatively easy time canceling the service successfully. Canceling was easier with LifeLock than with most ID theft protection services I’ve tested. I also was able to execute a hassle-free IdentityForce cancellation during my hands-on IdentityForce review.

Because LifeLock offers 24/7 customer service, cancellation is easier with LifeLock.

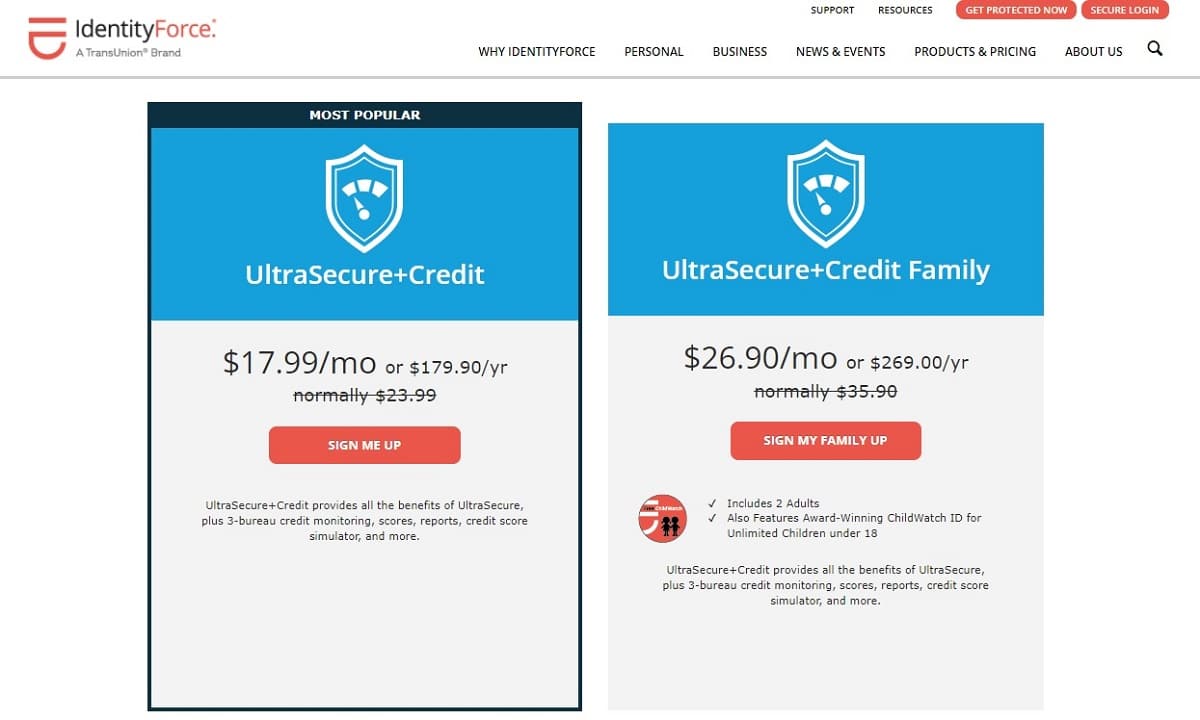

IdentityForce pricing tiers

IdentityForce has two pricing tiers, which greatly simplifies the process of deciding which tier you want to use. Both tiers offer a similar set of features as well, which is helpful for fully understanding what you’re receiving for your payment. The tiers include:

- UltraSecure+Credit: This tier works best for an individual. It delivers a high level of features, including three-bureau credit monitoring, reports, and scores; up to $1 million in identity theft insurance; 2FA; and stolen funds reimbursement.

- UltraSecure+Credit Family: This tier has all of the same features as the lower-priced tier, but it offers coverage for two adults on the account. It also includes ChildWatch ID for any children under age 18 in the family. ChildWatch ID monitors your child’s Social Security Number and other aspects of the child’s identity for fraudulent activity.

Unlike LifeLock, IdentityForce does not offer a money-back guarantee. Should you choose to try to cancel the service, you can request a reimbursement of any funds you paid ahead of time. However, actually receiving this reimbursement can be a significant challenge, as it is with many types of subscription services like this.

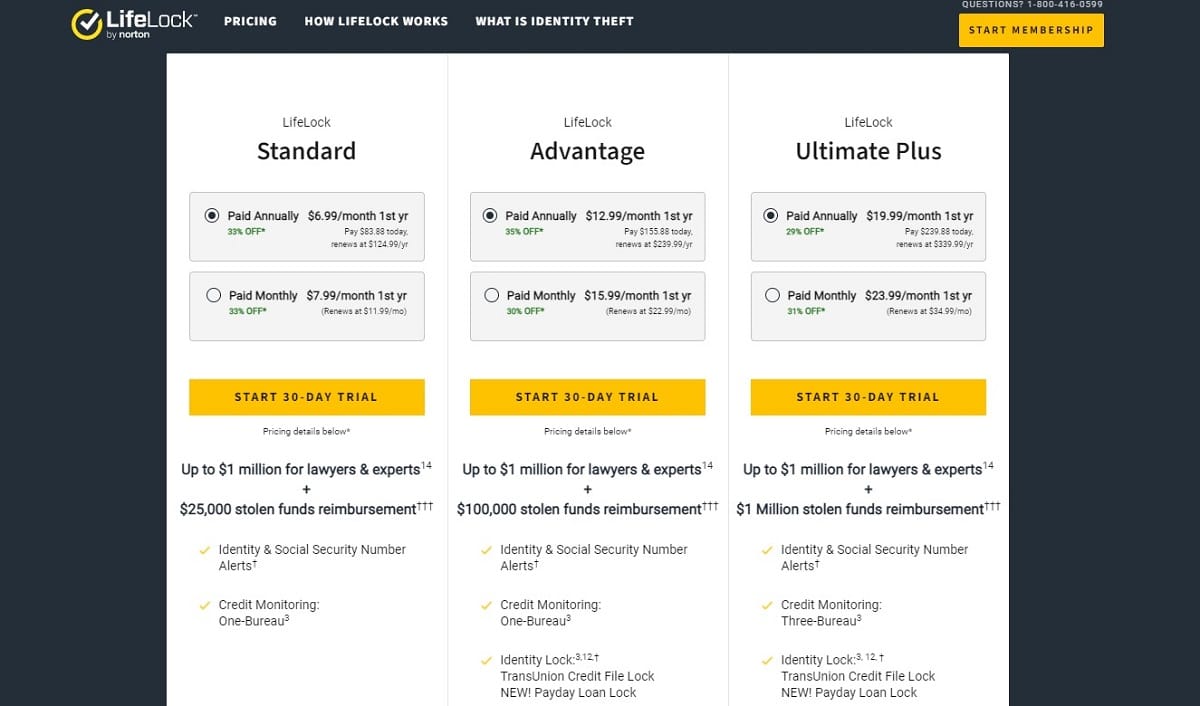

LifeLock pricing tiers

Compared to IdentityForce, LifeLock’s pricing tiers are far more complex. LifeLock has three pricing plans with three tiers within each plan, meaning you can select from any of nine different plans.

The three primary plans include support for an individual, for two adults, and for two adults and children. The tiers within each of those plans include:

- Standard: In the Standard tier, you will receive only basic protection, such as alerts related to identity risk and Social Security Number alerts. You will have access to identity theft insurance and stolen funds reimbursement. However, you only receive credit monitoring from one credit bureau.

- Advantage: The Advantage tier includes everything in the Standard tier, along with credit reports and scores from one bureau monthly. It also adds monitoring for crimes in your name and phone takeover monitoring.

- Ultimate Plus: In the Ultimate Plus tier, you’ll receive everything in the Advantage tier, as well as credit monitoring for all three credit bureaus. You’ll also receive unlimited credit reports from one bureau and an annual credit report from all three credit bureaus. This tier adds investment account monitoring and social media monitoring, which are not available in the low and middle price tiers.

Setup and ease of use

The signup and setup processes for both LifeLock and IdentityForce are pretty easy to use. You will be able to sign up for either service and begin using it within several minutes. As with most identity theft protection services, however, signing up and paying for the service is far easier than trying to cancel and receive a reimbursement down the road.

You will need to provide some sort of means of user identification, usually a driver’s license, as well as a credit card to sign up for either service.

The LifeLock dashboard contains quite a bit of useful information, and it has a nice level of organization. IdentityForce’s dashboard is also pretty well organized. I give LifeLock a slight advantage here in terms of ease of use.

Both IdentityForce and LifeLock offer mobile apps for iOS and Android. Both services will give you alerts through the app, which is helpful in notifying you as quickly as possible about a potential problem. LifeLock’s mobile app has a slight advantage in terms of its design.

Pros and cons of IdentityForce

Pros:

- Average cost is reasonable, especially for families

- Always offers credit monitoring for all three bureaus

- Ranks the risk to any of your data it finds on the dark web

- Uses a Credit Score Simulator that provides credit decision advice

- You’ll receive theft insurance up to $1 million in both pricing tiers

- Offers alerts through its strong mobile app

- Offers a free trial period

- Provides a nice collection of all-around protection

Cons:

- Fails to provide 24/7 customer service, unless you suffer a loss of your identity

- Doesn’t specify the exact maximum amount you could receive in theft fund reimbursement, which is odd

- Dashboard isn’t quite as easy to use as LifeLock’s dashboard

- Mobile app isn’t quite as detailed as LifeLock’s dashboard

Pros and cons of LifeLock

Pros:

- Delivers strong theft insurance and stolen funds reimbursement

- Mobile app is strong and provides immediate alerts

- LifeLock’s brand-name recognition greatly outshines competitors

- Norton owns LifeLock, and it’s one of the biggest names in computer security

- Offers many pricing tiers, so you can match the budget you have available

- Includes 24/7 customer service

- First-year pricing discount is significant

- Recently added a feature to monitor your account for payday loans

- Has a limited money-back guarantee

Cons:

- Second-year and beyond price increases are steep

- Both Norton and LifeLock have some poor customer responsiveness reviews

- Limits you to one bureau’s credit monitoring in the lowest-priced tiers

The winner: LifeLock

Although the differences in the IdentityForce vs LifeLock comparison are close, I found enough benefits in what LifeLock offers to give it the edge . LifeLock has more features and a more trustworthy brand name, giving it the slight edge, despite higher price points.

If you are a single user with very basic needs, or if you have a highly complex financial life, I would say LifeLock is definitely the better deal. It has a lower cost in its lowest-priced tier than IdentityForce, and it offers a few advanced features in its highest-priced tiers that IdentityForce can’t quite match.

I appreciate that IdentityForce provides more frequent opportunities to see your credit report from all three bureaus at all of its price points. LifeLock only gives you reports from all three bureaus at its highest-pricing tiers. IdentityForce’s credit monitoring features are more thorough as well, again using all three credit bureaus.

In terms of the types of personal information they monitor, both services are nearly identical. You do have to upgrade to LifeLock’s higher-pricing tiers to receive all of the features that IdentityForce offers in both of its tiers.

Even though both LifeLock and IdentityForce offer stolen funds reimbursement, LifeLock has an edge here. LifeLock offers maximum amounts ranging from $25,000 to $1 million, depending on the pricing tier you select.

IdentityForce’s stolen funds reimbursement numbers are not as clear. It offers up to $1 million as well, but it only says the maximum amount is available to certain pricing tiers. IdentityForce does not specify what its other maximum amounts are, which is a little unsettling.

If you aren’t quite sure whether identity theft protection services are for you, you will appreciate LifeLock’s limited money-back guarantee. IdentityForce does provide a free trial period, and it does offer to refund a payment you make in advance if you decide to cancel the service, but it doesn’t have a money-back guarantee.

I must mention here that receiving any type of refund with subscription services like this can be extremely challenging. If you decide you want to cancel, don’t expect to be able to send one email or make a two-minute phone call and cancel these services easily.

I also must point out that subscription services like this will generate significant amounts of marketing email and (potentially) texts once you give them your personal information. This can become overwhelming. Norton, the owner of LifeLock, is especially notorious for generating these kinds of notifications.

Ultimately, I believe LifeLock is a better choice for most people. It simply offers more features, and its well-known brand name gives customers confidence that it will deliver what it promises. IdentityForce has its advantages, though, and it may fit your situation better.

Our testing methodology for identity theft protection

When I’m researching the best identity theft protection services, I believe it’s important to approach the process from the point of view of the customer. I obviously cannot simulate every scenario that may apply to each reader, but I attempt to test the software in a way that works for the average consumer.

The ultimate purpose of the testing phase is to ensure that these services are living up to the promises they make to consumers. I also want to try to measure the ease of use of the software, ensuring that even someone who does not have a tech-savvy background can handle using it successfully.

The data I use with these services often involves simple entries meant to see how the software works. However, I also will enter some data meant to try to trigger alerts in the software. Through these tests, I hope to gain a feel for whether the theft protection software is performing as it should.

I also attempt to test the customer service responsiveness of these services. I want to give you the most accurate reflection of how these services respond when you have a simple question or when you need their help after you suffer a loss of your personal information.

In the end, for services that make the kinds of promises that identity theft protection providers make, I believe that these providers owe their customers the best service possible. They need to follow through on the marketing promises that they claim. Hopefully, my testing can give you some insight into the actual way these services work.

IdentityForce vs LifeLock FAQs

How does identity theft protection work?

Should your personal information end up in the wrong hands, you could suffer a significant financial loss. You could end up with a stolen identity, leaving you with months or years of work to try to regain your identity and to put your life back in order. When you subscribe to an identity theft protection service, the idea is that you will receive warnings and alerts any time your personal information is in danger of loss or theft.

If you suffer identity theft, the protection services should help you with restoring your identity. This can include filing legal documents required to try to restore the proper information to your identity profile and credit profile. The service should help you with disputing fraudulent transactions as well. After you suffer an identity breach, this personalized help is a vital aspect of these services, as most of us would have very little idea where to start on our own.

These ID theft protection services are not perfect. You could still suffer a loss of your identity if the exposure of your personal information is too extensive before the service figures out the problem. Your best chance at avoiding identity theft is to pay attention to danger signs and to be very careful about the information you share online.

Can LifeLock help me after someone stole my identity?

Should someone steal your identity, as a subscriber to LifeLock, you will receive help with attempting to recover your identity. LifeLock professionals will work with you to try to prevent the amount of damage that occurs to your identity and financial life. This will be a specialist based in the United States who can help you determine which information you need to file with the credit bureaus and with the government to work toward restoring your identity. LifeLock offers insurance protection to cover the costs of attempting to recover your identity of up to $1 million.

Can IdentityForce help me after someone stole my identity?

Yes. When you have information exposed on the internet, IdentityForce will provide up to $1 million of insurance coverage to attempt to help you pay for costs as you try to recover your identity. Professionals from IdentityForce will help you as well by communicating with the credit reporting agencies on your behalf to try to fix any errors in your information. Should you need to make legal filings to try to restore your identity, IdentityForce can help here too. IdentityForce can point you toward other professionals who can help, if needed.

Does LifeLock compensate me for stolen funds?

Depending on the subscription tier you are using, you could receive anywhere from $25,000 to $1 million in stolen funds reimbursement from LifeLock. You will have to produce some documentation about your losses.

Does IdentityForce compensate me for stolen funds?

Yes, but it’s not quite clear how much you can receive in your stolen funds reimbursement. IdentityForce offers coverage up to $1 million, but it also states that the maximum amount you could receive depends on the subscription tier you are using. It does not give additional information on exactly how much you could receive at each tier.

How can I protect my identity from being stolen?

Using an identity theft protection service can give you a better chance of avoiding having your identity stolen, but it’s not a guarantee. Outside of never sharing any information with anyone, which simply isn’t possible in the modern world, you always have a risk of stolen identity. The best way to reduce your risk of having your identity stolen includes never sharing personal information with any person or entity unless you completely trust that they are who they say they are. Don’t enter personal information on a web form after clicking on a random link in an email message and don’t give out information over the phone to a company or person that randomly calls you. These could be scams, meaning you could become the victim of ID theft by sharing information with someone pretending to be someone else.

Should I change my phone number after identity theft?

Changing your phone number is one way to protect yourself after having your identity stolen. Your old phone number could be part of your stolen personal information. If you open new accounts with that old phone number, you could end up being a victim again. Using a new phone number with your new accounts can provide one more layer of protection against suffering identity theft again.

Why would I want monitoring for all three credit bureaus?

Receiving credit monitoring from all three credit bureaus is an advantage when trying to protect your identity, because it is possible that the odd occurrence with your personal information may only appear at one credit bureau. If you don’t have access to all three bureaus for monitoring, you might miss this oddity, creating a delay that could leave your identity vulnerable.

Do credit cards offer identity theft protection?

IdentityForce and LifeLock offer a greater level of protection for your identity than what the credit card companies offer to their customers. Should you have an odd charge on your credit card, you can receive an alert from the credit card company to verify the charge. A few credit card companies will give you the option of receiving limited monitoring of the dark web for your personal information or of receiving access to credit reports. Typically, the credit card companies give you these services for free. Although these services from the credit card companies are helpful, they do not offer the depth that ID theft services offer.

Should I get ID theft protection?

This is not a one-size-fits-all answer. You could choose to perform all the services of the identification theft protection service on your own. You could access and monitor your own credit reports, and you could create alerts for odd occurrences for your financial accounts.

However, not everyone is comfortable doing these tasks on their own. For this reason and a few others, I believe certain types of people tend to receive a greater level of benefit from identity theft protection subscription services.

- Past ID theft victims: If you were a victim of identity theft in the past, you may have a greater chance of being a victim again in the future. The theft protection service can give you an early warning of another breach of your personal information.

- Those who dislike technology: To be able to monitor your own personal data and to keep an eye on your accounts, you need to be comfortable with accessing your account settings online. Elderly people or those who dislike using technology will often prefer allowing the identity theft service to do the account monitoring job for them.

- Those with very little time: If you simply do not have the time to keep up with your personal finance monitoring and credit reports, you may prefer paying the theft protection service to do this for you.

- Those who rarely need to check their credit: People who rarely use credit, such as children, may have no reason to regularly check their credit reports. Having an ID theft protection service monitor your credit for you may be helpful in this case.

One of the biggest selling points of ID theft protection software is the financial protection they offer to you. Should you suffer identity theft or should you suffer some sort of financial loss because of that theft, you could receive a payment to reimburse you for your losses and to cover your expenses related to trying to recover your identity.

However, I must mention that receiving these payments can be a challenging process. Even if you believe you have a clear-cut case and that you deserve a payment, the identity theft protection service may disagree. You may have to complete quite a bit of paperwork or speak with several customer service people to determine exactly what steps you have to take to qualify for reimbursement and payment. Ultimately, the ID theft protection services do not make it easy for you to obtain the payments you should have.

Additionally, once you sign up for one of these services, it can be extremely difficult to cancel the service and to stop payments. I would always recommend using a credit card to subscribe to an identity theft protection service, rather than giving the service access to your debit card or bank account. Should you want to cancel and should the service refuse to accommodate your request, continuing to charge your credit card, you may be able to contact your credit card company directly to put a stop to the payments.

Bottom line: Before you subscribe to an identity theft protection service, make sure you understand the potential pitfalls. Don’t just focus on the positives that the services brag about in their marketing materials.